Is Bitcoin money?

I've seen many attempts at answering this question but no good ones so far

Hi everybody, it’s been a little while. I spent some time last weekend writing about a question that keeps coming back to me.

Is Bitcoin money? I've seen many attempts at answering this question but no good ones so far.

This made me feel very unsatisfied and compelled to write to collect my thoughts. Let’s go ✍️

Most explanations of Bitcoin as money rush to give all kinds of common definitions of money, such as medium of exchange, store of value, unit of account, etc. They then make very specific explanations of how Bitcoin might (not) fit these categories. There's often a comparison to gold in there.

The problem with these explanations is that the world simply doesn't work this way. These explanations are too 'science-y'. Things don't become money because of scientifically categorised reasons. Things become money just because they become money. Money is a human concept. Human concepts can best be explained through humanities such as history, not science.

To say anything useful about the future of money, it's important to understand how money evolves (not why) and then apply this historical context to the future. Only then can we know if Bitcoin is money.

So how does money evolve?

Money evolves because people continuously do new things with a type of money, stretch it to its maximum, and then switch to a new money that suits their uses better. Let’s look at some examples and then turn to Bitcoin.

Coins as money

Before there’s coinage, there’s only debt. When people lived in tribes, they kept mental ledgers of who owed what to whom. As societies became more complex, these ledgers moved onto clay tablets. Inscriptions of debt on clay tablets from Mesopotamia precede the world’s first coins by thousands of years.

Coins break into the scene not to make these debt market places more efficient, but to defend them. Feeding an army in the ancient world represented a big problem. A camp of thousands of idle men would likely consume everything edible within 10 kilometers of their camp within a few days. Kings struggled to get villagers on their side. Slowly but surely, it became common practice to mint coins with the king’s face on it, hand them out to the soldiers, and then demand that every family in the kingdom was obliged to pay sone of those coins back to the king. Thus, entire kingdoms were turned into a vast machine for the provisioning of soldiers since every family, to get their hands on the coins, would need to contribute to general military efforts somehow.

When coins were introduced, people thought of them as debt for a long time. When the Pharisees ask if they should pay tax to Rome, Jesus points out that Caesar's head is on the coin and hence they should ‘give back to Ceasar what’s Ceasar’s’.

However, coins had new properties compared to debt. So people started doing new things with coins. One of these things was keeping more elaborate accounts. Often these accounts became so elaborate that they started to live a life of their own. In the 12th century, Charlemagne’s coin system - using pounds, shillings, and pence - was still used for record keeping 350 years after his death. Yet, some of these coins had never existed and none of these coins were still in circulation. Account keeping no longer required physical coins, but it had benefited greatly from their existence to standardise value over time.

Bank money as money

It makes sense that bank money would grow out of these medieval coin records. In the 13th and 14th centuries, coins came back to Europe as trade started picking up. However, there were so many different coins that banks emerged to facilitate trade. When a merchant would arrive in a new city, the first thing he would do would be go to a bank to exchange whichever coins he had for local paper bank money. People thought of this bank money as a claim on coins in a bank, exactly as written on the bank note.

However, bank money had new properties compared to coins and people started doing new things with bank money. One such thing was lending underlying deposits, especially to governments to field armies. The Medici were the first to discover the true power of banking, as they rose from common status to become the most powerful family in Europe at the time. Owning healthy banks meant access to finance, which directly translated into the power to win wars. States soon wanted this power for themselves, leading to the creation of central banks to supercharge national banking sectors and global financial empires. Banking power arguably reached its peak when JP Morgan’s loans to France and Britain effectively secured an allied victory in World War I. Bank money had become a thing of its own, only representing gold coins in a vault in name. The end of convertibility to gold in the 1970s merely confirmed a longer historical trend.

Bitcoin as money

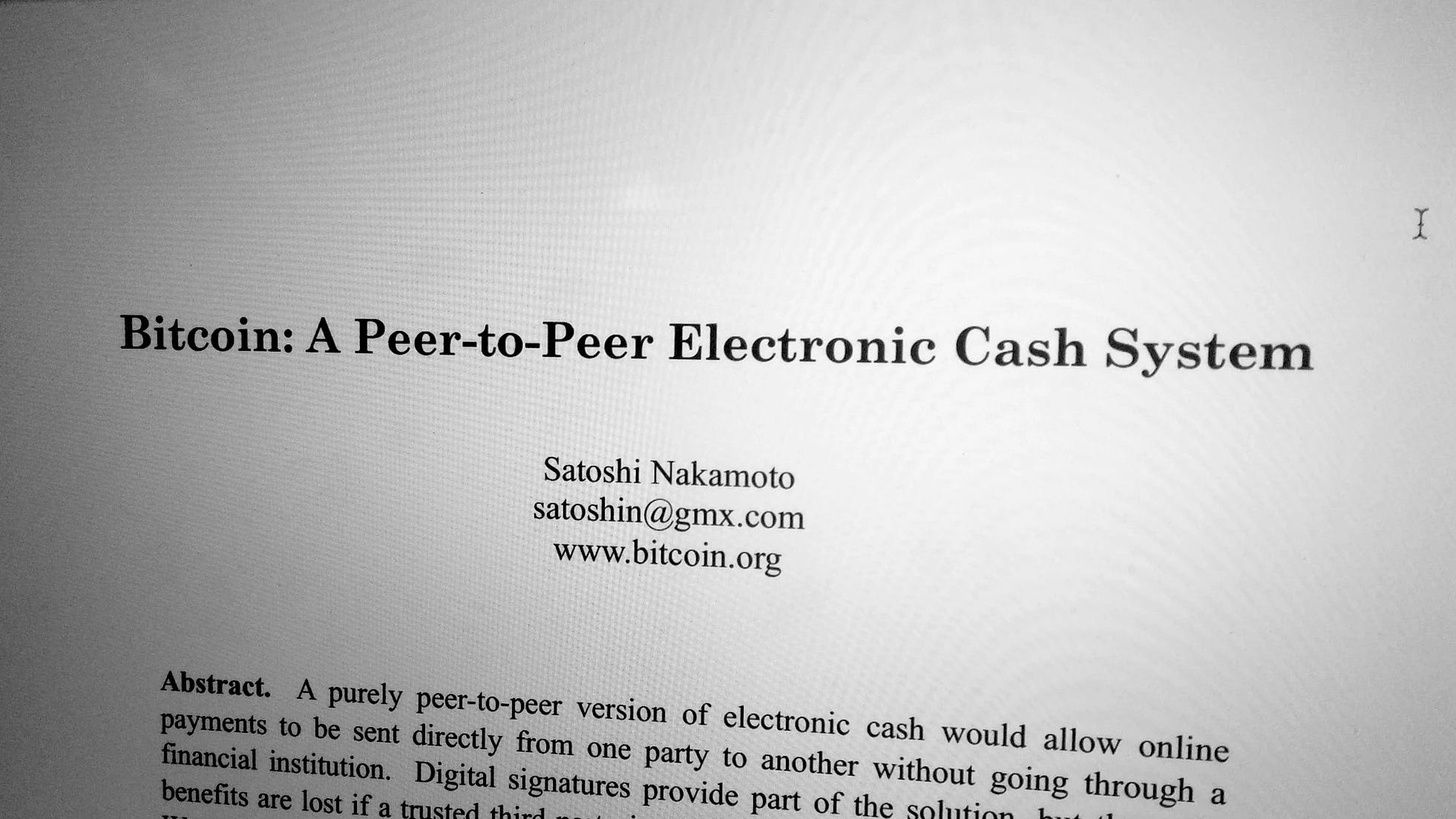

Since the 1970s bank money has become increasingly digitised. Satoshi invented Bitcoin in 2008 as a better alternative to bank money for a digitally native world. He writes about this in the introduction to the Bitcoin whitepaper, citing how “commerce on the internet has come to rely almost exclusively on financial institutions serving as trusted third parties to process electronic payments.” This is dominance of financial institutions leads to a practical problem according to Satoshi, namely that these institutions need to mediate in transaction disputes. Since the cost of mediation increases transaction costs, small transactions on the internet or money streaming becomes impossible. There’s a reason why you’re never paying less than ~$5 for your SaaS subscriptions - they aren’t viable because of how banks work.

So that means that Bitcoin is money? Well, if we’ve learned anything from the previous examples I would say that it’s only natural that we initially perceive Bitcoin as money. After all, coins were also perceived as debt first. And people thought of bank money as claims on gold (coins) too. However, Bitcoin introduces many new properties compared to bank money that mean that Bitcoin is much more than just money. Bitcoin will change our perception of money once again.

A bit further in the Bitcoin whitepaper Satoshi introduces Bitcoin as an electronic coin: “we define an electronic coin as a chain of digital signatures.” And he continues by saying that “each owner transfers the coin to the next by digitally signing a hash of the previous transaction and the public key of the next owner and adding these to the end of the coin” and that “a payee can verify the signatures to verify the chain of ownership”. If anything, Satoshi’s decision to use the word ‘coin’ is misleading. Bitcoin is nothing like any coin that we know. Rather, it is digital property. And digital property is a much broader category than just money. In addition, at the time of writing the chains of ownership that Bitcoin enables are secured by the largest decentralised computing network that the world has ever seen (thanks to Bitcoin miners).

If there are any lessons to be drawn from the history of money, it’s that new iterations on money derive their historical impact from their newness. Every time use cases emerged that were entirely unimaginable when it was first introduced. It would only make sense for the same to apply to Bitcoin. In a digitally native world, the most secure and decentralised computing network will be immensely impactful. As a result, Bitcoin is already so much more than money.

When we zoom out, it becomes clear that we’re in the early stages of something big. Change, however, doesn’t happen by itself. Change requires continuous work. At Trust Machines, we’re building the infrastructure to bring Bitcoin to its full potential as a decentralised computing network. And with Zest Protocol, we’re leveraging this infrastructure to build debt capital markets for the nascent Bitcoin economy. There’s an exciting future ahead!